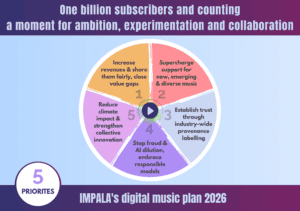

Reform of the digital music market to maximise revenues and opportunities for artists is one of IMPALA’s top priorities. Seeing music services as partners, IMPALA’s current plan is One billion subscribers and counting… A moment for ambition, experimentation and collaboration, adopted in June 2026.

More people listen to more music than ever before, and we are about to reach one billion subscribers on streaming services. This is something to celebrate. At the same time, there is significant potential for the digital market to become larger, fairer, more diverse and transparent. We focus here on streaming as it currently represents the biggest revenue source for recorded music, but these points apply beyond streaming, to the whole digital market.

In the spirit of partnership, and with shared goals to grow and develop the digital music markets which achieves its potential culturally, financially and sustainably, it is time to work together at a new scale of ambition. IMPALA’s proposals are aimed both at digital services as well as labels and distributors, large and small, independent and major, focussing on five priorities:

We build on previous recommendations which remain relevant, as well as recent analysis, including assessments of the evolution of a two tier streaming economy and the importance of diversity and independence in the music sector, by Dan Fowler, as well as the EU’s recent report on discoverability in Europe, which highlights multiple barriers that diverse European repertoire faces on digital services.

We welcome the widespread recognition in the sector that fraud and AI need collaboration and increased focus. A well-functioning market where genuine music flourishes and all attempts to game the system are stamped out is essential for all legitimate actors. At the same time, other priorities are equally important, and we believe have the potential to be transformative for the whole market.

As a result, there are multiple elements in our proposals, all contributing to the deep systemic changes needed to deliver better outcomes for all participants and build a healthy future. We test certain pre-conceived notions about how the digital music market should function. We also look beyond streaming to the digital music market as a whole, as we did in our previous proposals. Some recommendations can be progressed quickly, while others will require a sustained effort.

Underpinning our members’ views is the conviction that connections between artists and fans are at the core of digital music. We believe our five priorities are essential to effective growth across the whole digital music market, strengthening pluralism, fairness, diversity, trust, innovation and sustainability. In the annex of the plan, we set out what engagement with our recommendations would mean in practice for digital music services and also for labels and distributors:

What these recommendations mean for digital services

Increase revenues & ringfence: raise prices & rethink free tier, develop superfan tiers, no dilution of music royalties or price increases by other content, creator economy to develop new royalty strategies.

Make payment fair: stop thresholds, where retained, pay verified artists & distribute withheld monies differently, test alternative revenue models to support emerging artists & diversity.

Provide delivery flexibility: allow music to be withheld without penalisation where it is not monetised or otherwise well served & promote special features to boost competition.

Build stronger connections: employ human curators & editors, use artist-to-fan spaces & other features to engage fans & share data, strengthen presence in under-represented countries.

Commit to diversity: promote new releases, emerging artists & diversity in different forms (cultural, EDI factors, language, geography, genre), report yearly on concrete actions.

Deliver true discoverability: ensure authenticity, auditability, & transparency of factors affecting preferences & recommendations, eliminate rightsowner & financial bias.

Apply provenance labelling: agree industry-wide system to distinguish between artists signed to a record label (major/independent), self-released, library material, AI generated (tool used), other tags.

Stamp out fraud: collaborate with rightsowners on KYC, artist verification, metadata, fines & carriage fees, protective checks & balances to level playing field, stop artificial listening, revise sector code.

Protect human creation: stop dilution by genAI content (no royalties or discovery, work with rightsowners on responsible AI features for fans (eg DJ, mix), stop uploading unlicensed AI tracks.

Collaborate on sustainability: review ways to reduce impact collaboratively & transparently, report on different metrics (carbon per track stored, per play, impact of fraud & genAI content).

What these recommendations mean for labels and distributors

Establish provenance framework: labelling is an opportunity for discovery & integrity – artists signed to a label (major/independent), self-released, library material, AI generated (tool used) etc.

Clean the pipes: verify all music & each client, work with whole industry to update code on fraud & manipulation, help devise incentives with checks & balances that remove actors & protect good ones.

Apply multi-layered AI policy: publicly confirm rights are reserved for training, discuss with artists, agree industry definition & treatment of materially AI generated content, embrace responsible tools.

Promote diversity & connections: continue to invest in new releases & diversity, use features that engage fans, ask services for data, use IMPALA’s new EDI toolkit to measure as a business.

Pay fair royalties: pay fair contemporary digital royalty rates in line with WIN Fair Digital Deals Declaration, old contracts to be re-assessed, review relationships with social media & creator economy.

Share equity & other terms: advances, guarantees, sale of equity in DSPs etc, should be shared across artists represented/labels distributed, same for playlist & other commitments.

Ensure transparency: artist revenues must be clearly explained in agreements & royalty statements with a summary as well as sufficient detail to be understood.

Support session performers: where local industry wide agreements don’t exist for non-featured performer contributions, encourage negotiations on remuneration & terms.

Support sustainable choices: set targets & follow guidelines to reduce carbon & other impacts, measure with IMPALA’s calculator, communicate with fans, artists, suppliers, use climate investment facilities.

Lead sector innovation: continue to work on areas where innovative practices can improve the ecosystem, support new business models and practices, illustrate how the sector leads.

In June 2025, IMPALA had already published a report on « Combatting the emergence of a two-tier music streaming market », carried out by industry experts Dan Fowler and Katherine Bassett (statement here). who benchmarked the state of the digital market against IMPALA’s streaming plan as a set of KPIs for the industry. The report identified “five critical areas for immediate attention”:

- Combatting AI dilution and streaming fraud through cross-industry collaboration and regulation.

- Reforming royalty distribution models to ensure fair access for all market participants and increasing subscription fees in line with inflation.

- Enhancing transparency in DSP practices, especially concerning play-boosting tools and content de-monetisation.

- Restricting and reversing market consolidation to maintain competitive diversity.

-

Embedding consultation and impact assessment into any future industry changes to avoid unintended harm

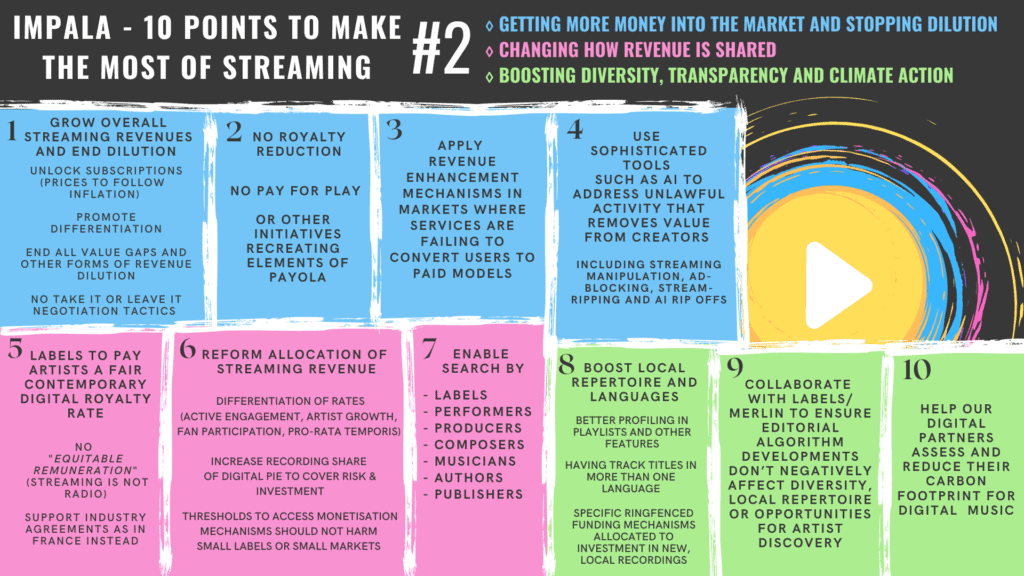

IMPALA first presented a streaming plan in 2021, building on work carried out by IMPALA’s digital and other committees. IMPALA’s second set of proposals called for increased subscription prices, fair digital royalty rates for artists, changes to how allocate revenues, bespoke deals for fans, and better valuation of master rights, among other proposals for a fairer, more dynamic market (infographic, It’s Time to Challenge the Flow #2 – Revisiting how to make the most of streaming). Our second call to action was featured in an op-ed for Billboard and since February 2024, thanks to WIN, our second plan has been available in 6 languages (English, Spanish, French, Portuguese, Japanese and Korean).

Since the release of our first plan, we saw various proposals from different parts of the market, echoing IMPALA’s original analysis. Five years later, despite closing in on 1bn subscribers, there is plenty of room for experimentation and collaboration to achieve ambitious change.

We continue to believe that modern revenue allocation models (such as Active Engagement, Artist Growth, Fan Participation and Pro-rata Temporis which we propose) are the answer, alongside fair contemporary digital rate to all artists, and industry-wide agreements (see the French example here). There are also renewed calls for User Centric, as has been recommended recently. There are no doubt other approaches that could be effective to counter both the “winner takes it all” trends and under-representation of different communities, genres, and countries.

Platforms and distributors must play their part in stamping out fraud and dilution by AI through industry wide collaboration. We must also work as a sector to increase the value of music and tackle all value gaps. Some platforms have initiated attempts to address this as well as streaming manipulation and impact of “noise” on music revenues. This we welcome, but these initiatives also raise issues that will have have negative impacts on the sector (see our replies to Deezer (here and here), Spotify (here), and Apple Music’s (here) proposals. Our current plan calls for thresholds to be stopped.

We also have points dedicated to enhancing diversity and addressing the vital question of sustainability and innovation. We have recommendations for services to really boost local markets in Europe, and we understand more about the carbon footprint of our entire industry now. Our carbon calculator is a key part of the independent sector’s programme for their emissions and we urge all services to do as much as possible and account transparently on how they handle their emissions for digital music.

Timing is important as there are increasingly calls for different approaches altogether, including more regulation. We see this as an opportunity to review and improve mechanisms, in order to pursue ambition, experimentation and collaboration, so we can take the lead. We will be assessing progress in the summer of 2027 and will ask our partners across the ecosystem to help us in doing this.

With our new plan, our previous recommendations remain relevant. For example, we questioned whether the master right share for artists and labels is being undervalued given the market assessments in the UK. Addressing this question is crucial for investment in new talent to continue, especially with back catalogue continuing to dominate music consumption in general.

This is also why we confirm commitments for modern digital royalty rates and ask labels and distributors to shre equity and other forms of remuneration across all artists/labels distributed. We also continue to oppose so-called “equitable remuneration” (for performers to negotiate with services for a parallel fee – for more on IMPALA’s position on this see here), which would reduce capital for investment in new artists and projects and would not result in greater pay-outs to artists. This also links to our work on equity, diversity and inclusion, which is flagged in the section on “cutting the digital pie – what is equitable” in IMPALA’s second annual report on this area. Ben Wynter – former AIM Entrepreneur and Outreach Manager, co-founder of POWER UP and founder of Unstoppable Music Group sums up his views on streaming reform and equitable remuneration: “We need to ask ourselves what the long term effect will be on business, investment, creativity and innovation. For example “equitable remuneration” would inevitably lead to smaller label advances and lower royalty rates, which disproportionately affects certain groups. We need more resources for investment in new artists and projects, not less. We also need to think about artists who prefer to own their rights. Exclusive rights are essential for artists and labels and trying to pour everyone into a single mould is simply not an inclusive approach.”

Timing is important as there are increasingly calls for different approaches altogether, including more regulation. We see this as an opportunity to review and improve mechanisms, in order to pursue ambition, experimentation and collaboration, so we can take the lead. We will be assessing progress in the summer of 2027 and will ask our partners across the ecosystem to help us in doing this.

For backround, our ten points from 2023 are below and IMPALA’s full paper is available here: It’s Time to Challenge the Flow #2 – Revisiting how to make the most of streaming (2023)

Click here for the 10-point in infographic form (2023).

IMPALA’s statement on the day of publication is here.

The IMPALA 10-Point Plan to Make the Most of Streaming (2023)